Being busy isn’t the same as being profitable. Knowing how to price HVAC jobs is key to turning full calendars into sustainable businesses.

A lot of shops price from wages and parts, then wonder why profit stays thin. The missing piece is the true cost of delivering the work: fully burdened labor, overhead and the small leaks that never show up on the estimate.

A $20 capacitor can feel like easy money at $150. But once you include labor burden, vehicle and drive time costs, plus overhead, the real cost of that “quick” call can land higher than the invoice.

This HVAC pricing guide breaks pricing into three practical stages for simple residential and straightforward HVAC service work. Along the way, you’ll see how Simpro® helps teams capture the job-level data that makes pricing more consistent and more profitable over time.

If you’re building estimates for larger commercial, construction, or complex bid work, check out our guide on how to bid HVAC jobs.

Calculating Core Job Costs

Before you decide what to charge, you need to know your floor: the absolute minimum a job must bring in to avoid losing money.

Most pricing problems are visibility errors. Costs get left out, assumptions creep in, and small gaps compound across dozens of service calls each week. Unbillable time, unapplied labor and inventory shrinkage rarely show up on an estimate, but they always show up in your P\&L.

Your pricing floor rests on three pillars:

- Fully burdened labor

- Materials with structured markup

- Overhead allocated across real billable hours

If any one of these is understated, every pricing model built on top of it becomes unstable.

Let’s start with the largest cost driver: labor.

Defining and Calculating Fully Burdened Labor Costs

You may already understand that a technician’s hourly wage is not their hourly cost.

Fully burdened labor includes everything required to put that technician in a truck and on a job site: employer payroll taxes, workers’ compensation, health benefits, retirement contributions, paid time off, training and certifications, uniforms, phones, and the labor-related portion of vehicle expenses.

A simple framework looks like this:

Fully burdened hourly cost = Total annual employment cost ÷ Total annual billable hours

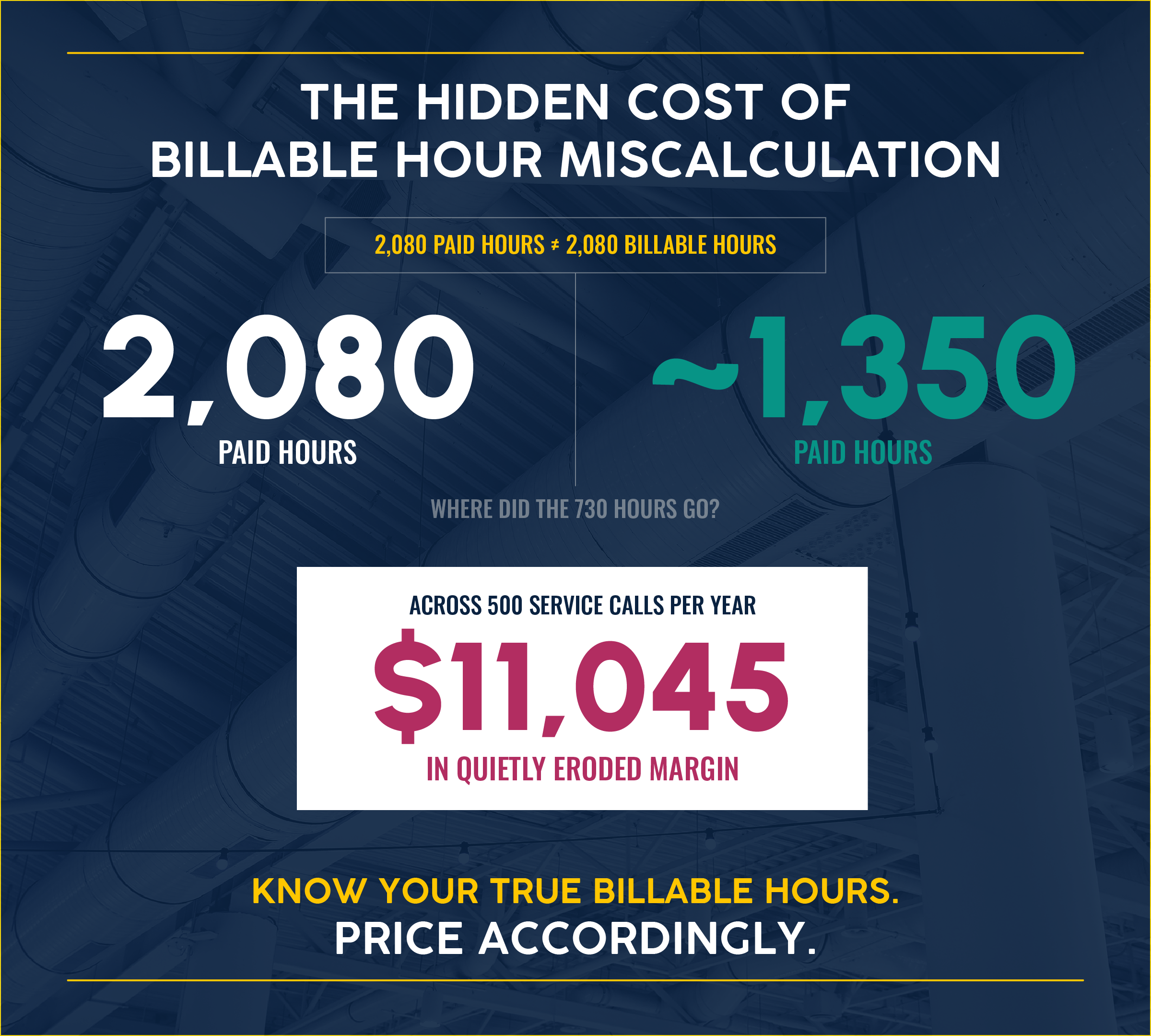

The total employment cost is usually straightforward once you gather payroll and benefits data. The billable hours is where many shops miscalculate.

Full-time technicians may be paid for 2,080 hours a year, but that doesn’t mean they bill 2,080 hours a year.

Drive time between jobs, loading and restocking trucks, callbacks, meetings and training are all real costs. If you divide annual employment cost by paid hours instead of actual billable hours, you under-recover labor on every single job.

That under-recovery doesn’t feel dramatic, but multiplied across hundreds of service calls, it quietly erodes margin.

For a detailed walkthrough of the labor burden rate formula with calculators, check out our labor burden rate calculator.

Even with the right formula, labor burden falls apart when your time data is incomplete. Manual and paper-based tracking leads to wage leakage, unverified overtime and blurry billable versus unbillable hours.

Blue Wave Communications had relied on handwritten timesheets, a familiar problem for any shop running paper-based time tracking. After shifting to digital field entry, they reduced overtime costs by 75–80% and cut payroll processing from multiple days down to multiple hours.

Simpro Mobile Timesheets let technicians log exact start and finish times on their devices while on site, tied to the job card. In System Setup, you can build schedule rates that include overhead and employment cost multipliers, then technicians select the appropriate rate and log actual time against the job. Back in the office, the Schedule Breakdown and Timesheets modules reconcile actual hours against payroll and job costing, so your labor burden calculation is built on actuals, not rekeyed notes or best guesses.

Material, Equipment, and Parts Costs

Material cost and sell price are two different numbers connected by markup. The key is that markups should be tiered: lower on high-ticket equipment where customers are price-sensitive, and higher on small parts where handling and logistics costs are proportionally larger.

The core formula is straightforward:

Total material sell price = (wholesale cost + tax) × (1 + markup percentage)

But this is where “right math” can still steer you wrong. A markup is a percentage of a known cost. The moment your cost data becomes disconnected from live supplier pricing or your inventory count becomes inaccurate, you’re applying markup to the wrong number.

That’s how you end up doing the work, sending the invoice, and still coming out behind.

Silent shrinkage: the invisible profit killer

The ACCA (Air Conditioning Contractors of America) sets acceptable inventory shrinkage at 10% or less for HVACR companies, a standard that can be challenging for many businesses to achieve.

Material margin usually leaks in two places:

- Internal leakage: Truck stock gets consumed in the field but is never logged against the job. The part leaves inventory, the job card stays clean, and your invoice goes out light.

- External overcharges: Supplier invoices don’t match the agreed pricing or purchase order. The difference might be small on any one invoice, but across volume it adds up fast.

Markups protect you from expected costs. They don’t protect you from untracked usage or supplier pricing drift.

Allocating Business Overhead

Overhead is everything your business spends that isn’t tied to a specific job: rent, utilities, office staff salaries, insurance, marketing, software subscriptions, vehicle payments and general administrative expenses.

Those costs don’t pause when a technician is on a call. They have to be distributed across your billable hours so every job contributes to keeping the business running.

HVACR Business expert Ruth King notes that overhead cost per hour should ideally be under $40/hour for service work and under $30/hour for installation, though many companies actually exceed $60/hour. Small HVAC shops typically average 30–40% overhead as a percentage of gross revenue.

A simple formula looks like this:

Hourly overhead rate = Total monthly overhead ÷ Total monthly billable hours

Many HVAC businesses treat overhead as a fixed tax, something unavoidable but disconnected from pricing decisions. However, overhead is tightly linked to workflow. If your processes are manual, growth often forces you to add office staff just to keep up with scheduling, job updates, follow-ups and invoicing.

This is the growth trap.

Revenue increases, headcount increases, overhead per billable hour stays flat, and profit margins stall.

McCarthy Plumbing Group experienced the opposite. After implementing workflow automation, they doubled their yearly revenue without hiring excess administrative staff to fill operational gaps, avoiding an estimated $750,000 in projected salary costs over five years.

Selecting the Right HVAC Pricing Strategy

Once you know your cost floor, the next decision is how to present that price to the market.

Different jobs require different pricing models. The right model balances customer trust with company risk. Most HVAC service work falls into one of three categories:

- Flat-rate pricing

- Time and materials (T\&M)

- Hybrid pricing

Each has a place, and you want to carefully consider the financial trade-offs.

For a deeper dive into structuring tiered proposals, see our guide to building a good-better-best HVAC proposal.

Flat-Rate Pricing Mechanics

Flat-rate pricing means quoting a single fixed price for a defined scope, regardless of how long the job actually takes. Labor, materials, overhead and profit are bundled into one number.

It works best for routine maintenance, predictable repairs and standard installations. Jobs where scope and duration are consistent.

The structure looks like this:

Flat-rate price = (estimated labor hours × hourly rate) + (estimated materials × markup)

The advantage to this method is clarity. Customers know the price upfront. Billing disputes decrease. And when technicians work efficiently, the margin improves.

However, the risk sits on your side. If the job takes longer than estimated, margin shrinks.

Flat-rate pricing only works when your pricebook is a living document. If you aren’t comparing estimated times against actual field data, you end up pricing based on how long a job should take, not how long it does take your specific team or technician.

Audem Electrical discovered a systemic underpricing issue firsthand when analyzing its operations. Data revealed they were losing money on a specific job type (small air conditioning installations) without realizing it. Standardization corrected that through Simpro’s Pre-Builds and pricing tiers.

Time and Materials (T&M) Mechanics

Time and materials pricing bills the customer for actual labor hours and materials used. It’s the risk-protection model for unknown scope, complex repairs, emergency calls and custom retrofits where quoting a fixed number would require guesswork.

The structure is simple:

Total cost = (actual hours worked × hourly rate) + (materials cost × markup)

On paper, T&M is the safest pricing method because every dollar spent is billed.

In practice, it introduces a new risk: billing lag.

If it takes weeks to translate handwritten field notes and receipts into an invoice, you are effectively financing payroll, materials, and overhead until that invoice goes out.

Enhanced Electrical experienced this friction. Previously, T&M jobs had to be manually calculated, leading to administrative delays and lost revenue. After digitizing job capture and invoicing workflows, they reduced invoice generation time from four to six weeks down to just a few days.

Hybrid Pricing Mechanics

Some jobs don’t fit cleanly into flat-rate or T&M.

A residential HVAC job might include a predictable AC tune-up plus custom duct modifications. One portion can be confidently priced as flat-rate. The other carries variable scope and risk.

Hybrid pricing separates those components.

Total cost = flat-rate portion + T&M portion

The challenge is tracking it.

If you treat the entire job as a single bucket, the T&M portion can quietly eat into the margin built into the flat-rate portion. Without granular tracking, you won’t know where the leak began.

Enhanced Electrical increased profitability by 5X after breaking jobs into separate cost centers and tracking performance independently.

For more context on structuring your job estimation workflow around these pricing models, our estimation guide walks through the process end-to-end.

Finalizing Price and Profit Margins

You’ve calculated your cost floor. You’ve chosen the pricing model. Now comes the hard part: converting cost into a sell price that hits your target margin and defending that margin while the job is in motion.

Calculate Target Profit Margins

Markup is a percentage of cost. Margin is profit as a percentage of the selling price. Confusing the two is one of the most common pricing errors in HVAC.

Here’s the correct formula:

Selling price = Total cost ÷ (1 − Desired profit margin)

Example:

If a job costs $100 and you want a 30% margin, the correct sell price is:

$100 ÷ 0.70 = $143

Selling it for $130 achieves a 30% markup but only a 23% margin.

Conflating the two, alone, can flatten profitability.

For more details on the distinction and how to apply it to your HVAC business, see Simpro’s guide to HVAC profit margins.

Check Against Industry Benchmarks

While results vary by market and business model, general industry benchmarks suggest:

-

Commercial HVAC margins often range from 5–15% net

-

Residential HVAC margins typically target 15–20% net or higher

-

Gross profit margins often fall between 30–60%, depending on the department

Small contractors frequently land closer to 5–7% net. Larger, well-structured companies often reach 8–12%. Top-performing contractors can achieve 15–25%.

The gap between those ranges is cost control and pricing precision.

Close the Gap Between Targets & Reality

The second the job starts, reality begins chipping away at your margins. If you only look at your margin in a monthly P&L, you’re too late.

Simpro helps move visibility forward. The Breakdown Table and Projected Financial View show estimated costs alongside actual costs inside the job’s Summary tab before invoicing. Values highlight when actuals exceed budget, allowing teams to intervene while the job is still active.

Pricing precision only works when margin is monitored in real time.

Structuring Taxes and Fees

Taxes and fees are variables that can quietly distort your pricing if you don’t handle them deliberately.

Most HVAC businesses list sales tax as a separate line item on quotes and invoices. It keeps tax rate changes from eating into margin, makes the math cleaner for customers, and simplifies compliance.

Fees work the same way. Diagnostic charges, dispatch fees, after-hours premiums, and permit-related costs are easiest to manage when they’re clearly defined and consistently applied. The goal is transparency without giving away margin.

Don’t let taxes and fees become last-minute adjustments that undermine the price you meant to charge.

Pricing Memberships Without Eroding Margin

Maintenance memberships are one of the strongest levers for long-term profitability because they create predictable scheduling and repeat revenue. But memberships only help if the discount logic is engineered into your pricebook.

Build discounts into the baseline

Membership discounts (often 10–15% off repairs) should be built into your standard pricing.

- Set your member price at your target margin

- Set your non-member price 10–15% higher as a premium rate

- The member rate becomes the “true” price

- The non-member rate becomes the bonus

This way, the discount doesn’t erode margin because it’s already accounted for.

Typical HVAC membership programs include three tiers.

For example:

- Basic tier: $99–$149/year (one to two tune-ups, 5–10% repair discount)

- Standard tier: $149–$249/year (two tune-ups, ~15% discount, priority scheduling, waived diagnostic fee)

- Premium tier: $249–$399/year (standard perks plus 20% discount, equipment replacement credits, extended warranty coverage)

Memberships are a volume play, so admin efficiency matters

Membership programs scale through volume. But if adding 500 members means hiring another office person to manage billing and scheduling, predictable revenue gets swallowed by overhead.

Any trade business running recurring service programs hits the same wall. Coastal Security, which operates maintenance contracts at volume, automated 75% of its billing and saved more than 40 hours per week in back-office work. The dynamic is identical for an HVAC shop scaling a membership program: the overhead you just controlled gets added right back if the billing and dispatch aren't automated.

Simpro’s Memberships, Recurring Jobs, and Simpro Payments features handle this at scale. You configure the membership in System Setup, set up recurring job templates linked to each customer, and activate the Customer Portal with Simpro Payments so customers can pay online. The result is a membership program that scales without a corresponding increase in admin labor—keeping the overhead you worked so hard to control in check.

Pricing for Profit

Most HVAC businesses don’t lose margin because they’re bad at the work. They lose it because pricing is built on partial information: a wage rate instead of a fully burdened cost, a markup applied to outdated part pricing, overhead allocated to “typical” hours instead of real billable hours.

If you want pricing you can defend, don’t start with what competitors charge. Start with what the job actually costs you to deliver, then choose the pricing model that fits the scope and risk.

The goal isn’t to add mind-numbing administrative work. It’s to stop guessing.

When time, materials and job costs are captured where work happens and reviewed while the job is still active, pricing becomes consistent, margins become predictable, and growth stops feeling like a gamble.

For more on pricing across the trades, learn how Simpro helps field service businesses turn pricing precision into sustained profitability.