Whether you're a small business or a larger enterprise, preparing for the End of Financial Year (EOFY) can make all the difference when it’s time to lodge your taxes.

In the world of trades and field services, there are many moving parts. From reviewing records and claiming the right deductions to meeting deadlines, there are ongoing projects, fluctuating costs, equipment depreciation, and more.

To help you navigate this alongside your tax obligations, we've compiled the ultimate guide on how to prepare for the UK’s EOFY, all year round.

When is the EOFY in the UK?

The EOFY (sometimes called Accounts Reference Date) marks the end of a financial year; a business’ accounting period affects the deadlines for paying Corporation Tax and filing a Company Tax Return. The UK government follows a fiscal year from 1 April to 31 March. However, the EOFY can differ depending on the type of entity you’re running. Here's a breakdown:

- Sole traders and personal tax year runs from 6 April to 5 April of the following year.

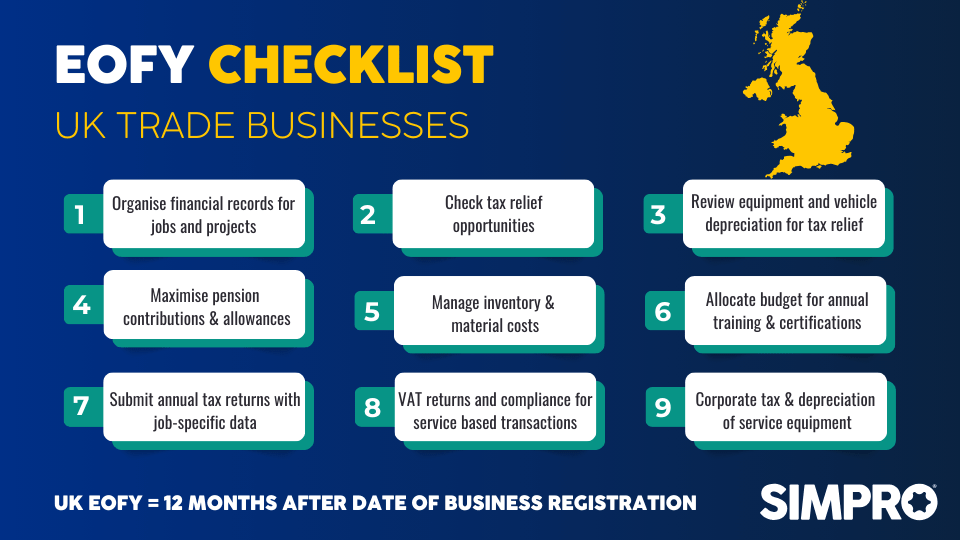

- A company’s financial year usually ends 12 months after the date of incorporation (business registration). If your first set of accounts spans longer than 12 months, you may need to file two tax returns to cover the period for the first year. This means you'll also have two payment deadlines. Companies can request to change their financial year-end date with the His Majesty’s Revenue and Customs (HMRC), so businesses across the UK may have different EOFY reporting periods.

- The Corporation tax accounting period typically matches the company’s financial year or association’s annual accounts and can’t exceed 12 months. If a business changes its financial year-end, it’ll likely need to adjust the corporation tax accounting period.

For field service businesses, thinking strategically about when your EOFY falls is useful. Aligning it with a slower period might help you manage your cash flow and workload.

Important UK financial and fiscal year dates for businesses

Keeping track of important dates is essential. Plan ahead to help you avoid late penalties and ensure you file everything on time.

Here are the key dates you need to know:

- 31 March: The end of the government fiscal year. This matters if you do business with public sector clients.

- 5 April: The end of the personal tax year. This is a crucial date for sole traders.

- Corporation Tax Deadline: You must pay your corporation tax nine months and one day after the end of your accounting period. For example, if your financial year ends in December, your corporation tax will be due by 1 October of the following year.

- VAT Returns: Your VAT deadlines will depend on whether you're on a quarterly or annual VAT period. Usually, these are submitted one month and seven days after the end of the VAT quarter.

How to decide your company’s financial year

By default, a company’s financial year ends 12 months after its incorporation date. For example, if your business was incorporated on 1 June 2023, your first financial year would run until 31 May 2024.

In the UK, businesses can change their financial year-end to better align with their operations. Shifting your EOFY can help with cash flow management and tax deferral, particularly if you want to avoid managing tax payments during peak periods. Note that changing your year-end date will affect your tax reporting dates so it’s important to consider the best time for your business to undertake this work.

While businesses can change their financial year-end, they can only do so once every five years. According to UK tax experts Westwon, March and December are among the most common months for companies to close their financial year, as these months often align better with business cycles, allowing smoother transitions.

If you're considering changing your reporting dates, it’s important to weigh the pros and cons and inform HMRC accordingly.

6 steps to prepare for the EOFY in the UK

Preparation is key to success. There are simple ways to ensure your business benefits from EOFY obligations. By sorting everything before the EOFY, you’ll streamline the process and minimise the risk of errors or missed deductions. Here are six steps to prepare your field service business:

1) Organise financial records for jobs and projects

Field service businesses tend to have many moving parts:

- ongoing projects

- job-specific expenses

- invoices, and receipts.

Make sure all your financial records are well-organised before you close your books for the year. This includes sorting out job-specific costs such as labour, materials, and equipment usage.

Save time by keeping accurate and up-to-date records when filing tax returns and reviewing your financial performance.

2) Check tax relief opportunities

The end of your fiscal year is an ideal time to review available tax reliefs that can help lower your tax bill. From capital allowances, charity donations and government-led incentives, your business may be eligible for valuable tax reliefs and allowances.

For example, if your business has undertaken research and development (R&D), you could be eligible for the merged scheme R&D expenditure credit (RDEC) and enhanced R&D intensive support (ERIS), offering a financial boost.

3) Review equipment and vehicle depreciation for tax relief

For businesses in the field service sector, equipment and vehicles are often your largest assets. Depreciation on these assets can be used to reduce your taxable profits. If you’ve invested in equipment or vehicles, ensure you’ve recorded depreciation accurately – this can lead to significant tax relief.

Businesses can claim Annual Investment Allowance (AIA) to deduct the full cost of certain capital assets, like machinery, in the year they are purchased.

4) Maximise pension contributions and allowances

EOFY is also a great time to review pension contributions. Employer contributions to pensions are tax-deductible, so if you haven’t reached the annual allowance, consider if making additional contributions could be beneficial.

5) Manage inventory and material costs

Field service businesses often rely on significant materials and inventory. To ensure you claim the right deductions, accurately account for your inventory. If you use the stock relief method, regularly stocktake to avoid over- or under-stating your expenses.

6) Allocate budget for annual training and certifications

If you’ve identified your workforce could benefit from training and professional development, ensure you account for these expenses. Training costs are often tax-deductible, so budgeting for them as part of your EOFY planning can be a smart financial move.

EOFY reporting obligations for UK businesses

Businesses have several reporting obligations at the end of the fiscal year. Let’s break down what you need to do:

Submit annual tax returns with job-specific data

Your business will need to submit an annual corporation tax return. This includes income from all jobs, as well as the costs associated with those jobs. Record all expenses thoroughly, as this will reduce your taxable profit. You can also reduce the manual effort with time-saving digital tools, such as job management and job costing software.

VAT returns and compliance for service-based transactions

If your field service business is VAT-registered, you’ll need to ensure your VAT returns are up to date. This means accurately tracking VAT on both sales and purchases. Service-based businesses can sometimes find VAT tricky, as it depends on the type of service you provide, so make sure you comply with HMRC's guidelines.

Corporation tax and depreciation of service equipment

Don’t forget about depreciation on vehicles, equipment, or any other capital assets used for your service-based business. You can claim tax relief on depreciation, which will help reduce your overall corporation tax liability.

Streamline the EOFY process with software

Simpro’s field service management software streamlines your operations, from invoicing and inventory management to detailed reporting, making EOFY preparations smoother and more efficient. Connecting your field teams with the office in real-time enables seamless tracking of payments and invoices.

EOFY reporting tip from Simpro’s partner , Tugger:

Make your End of Financial Year reporting smoother by connecting Simpro to Power BI with Tugger. This setup allows you to automatically update and visualise your data in customised dashboards, giving you clear insights into project performance, budgets, and resources. It’s a simple way to save time on manual reporting and make sure your decisions are based on up-to-date, accurate information.

- Craig Morrall, Tugger

Simpro reduces double-handling, saves time, and streamlines your EOFY preparations, helping you achieve a more efficient and stress-free fiscal year-end. Explore Simpro’s features:

Business and financial reporting tools

Take control of your finances with detailed reports, job costing and configurable dashboards that provide an in-depth view of your financial performance.

Accounting integrations

Integrate seamlessly with your cloud accounting software to ensure accurate, transparent financial data that stays synchronised across all systems.

Cash flow management

Efficiently estimate, invoice, process payments, and track profitability. Improve your field service cash flow and gain clear visibility into your business’s financial health.